We all know that one of the reasons people open Health Savings Accounts is the triple tax advantage, which, simply stated, means:

- HSA contributions are tax free

- HSA earnings grow tax free

- HSA distributions for qualified medical expenses are tax free

However, there is a hidden fourth tax advantage to HSA’s that is not widely known, and can save you money. The fact is that HSA contributions can be payroll tax deductible as well. In the term “payroll tax” I lump the various taxes often described as FICA taxes which include Social Security, Medicare, and Unemployment Insurance. This is on top of the exclusion to income tax as shown in #1 above.

How to avoid Social Security and Medicare taxes an with HSA

There are various ways to contribute to an HSA which include:

- Post-tax contributions

- Pre-tax contributions

- Employer Contributions

- Qualified Funding Distribution (from IRA)

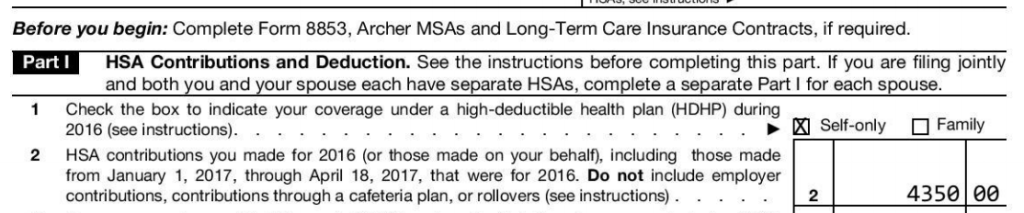

The main method people use to contribute to their HSA is #1 above, via post-tax HSA contributions. This involves depositing money into your HSA from your bank account using dollars you previously paid taxes on. Unfortunately, since those dollars likely came from an employer you would have already paid income, social security, and Medicare taxes. The income tax will be “returned” to you when you file Form 8889, but the Social Security and Medicare taxes are gone and cannot be credited back. In this way, you cannot avoid Social Security or Medicare taxes with a post-tax contribution.

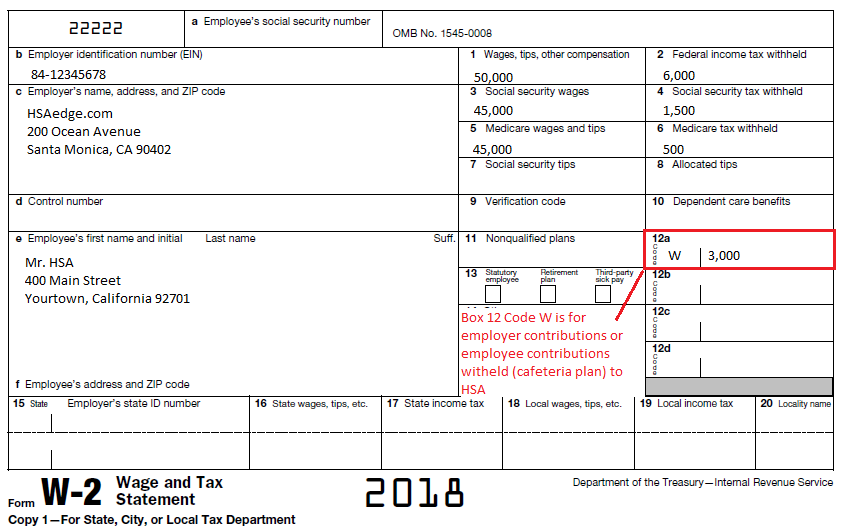

The good news is you can avoid paying Social Security and Medicare taxes using pre-tax contributions. Pre-tax contributions are contributions withheld from your paycheck by your employer and deposited into your HSA for you. This often takes the form of a Cafeteria Plan, which is an automated contribution plan on behalf of the employee. This is an important distinction, because per IRS Form 15, only pre-tax contributions using a cafeteria plan can avoid Social Security and Medicare taxes:

However, HSA contributions made under a salary reduction arrangement in a section 125 cafeteria plan aren’t wages and aren’t subject to employment taxes or (Social Security, Medicare) withholding.

They distinguish that from a “payroll deduction plan” which, while undefined, is likely looser and does not meet the same requirements as a section 125 deduction. The result is you have to be using a section 125 cafeteria plan to make a pre-tax contribution that avoids these additional taxes. Your employer will have more information about this but is likely using this vehicle since it is most advantageous for both the employee and the employer. Contributions made in this way will be deducted from your paycheck before income, Social Security, and Medicare taxes are paid. In this way you save that money and it goes into your HSA instead of being paid to the government. As we will see, this can be a significant amount of money.

How much FICA taxes can you save with an HSA?

Here is a theoretical example of how much you can save on FICA taxes in addition to regular income tax using cafeteria plan HSA contributions. For 2017, you are taxed 6.2% of your income for Social Security up to a salary limit of $127,200. In addition, Medicare is taxed at 1.45% of wages with no ceiling.

Let’s say that for 2018, you have Family HSA insurance which has an (ever-changing) contribution limit of $6,900. Let’s say that you make contribution the family maximum using post-tax dollars. As mentioned, there is no way to avoid Social Security and Medicare Taxes on these amounts. Thus, you will pay:

| Post-Tax | Cafeteria Plan | |

| Contribution | $6,900 | $6,900 |

| Social Security (6.2%) | $427.80 | $0 |

| Medicare (1.45%) | $100.50 | $0 |

| Total: | $528.30 | $0 |

Contrast that with the cafeteria plan, contributions to which avoid these two taxes.

In addition to this, your HSA contribution might save you on various state taxes as well. Many states remove HSA contributions from state tax calculation. One notable exception is are tax hungry states like California who does not allow HSA contributions to be deducted from state income tax. Either way, state taxes for things like Disability and Unemployment insurance can range from 1-2%, so that is another $75 to $150 right there.

How employers save on taxes with an HSA Cafeteria Plan

It is also in an employer’s interest to establish a cafeteria plan for employee’s HSA contributions. This is because employers must also make a contribution to Social Security and Medicare coffers on behalf of the employee. While the employee contributes 6.2% and 1.45% percent of salary (up to limits for SS) to the government, the employer must make the same contribution for employee’s salary. That means that for each dollar you are paid, 12.4% is going to Social Security (6.2% + 6.2%) and 2.9% is going to Medicare (1.45% + 1.45%). This results in a tax of 15.3% going to the government for each dollar you ear.

The cafeteria plan deduction offered to employees also extends to the employer. So employer Social Security and Medicare contributions are not required for employee contributions made through a cafeteria plan to an HSA. So the same example applies, for each employee contributing $6,900 to an HSA via cafeteria plan, the employer can save $528.30 in taxes. Per IRS Form 15:

Your contributions to an employee’s health savings account (HSA) aren’t subject to social security, Medicare, or FUTA taxes, or federal income tax withholding if it is reasonable to believe at the time of payment of the contributions they’ll be excludeable from the income of the employee.

Note: if you need help with your HSA taxes this year, please consider using my service EasyForm8889.com to help complete Form 8889. It is fast and painless, no matter how complicated your HSA situation.